Publications

Working Papers

- A Generalized Additive Partial-Mastery Cognitive Diagnostic ModelCamilo A. Cárdenas-Hurtado, Yunxiao Chen, and Irini MoustakiNov 2025

Cognitive diagnosis models (CDMs) are restricted latent class models widely used for measuring attributes of interest in diagnostic assessments in education, psychology, biomedical sciences, and related fields. Partial-mastery CDMs (PM-CDMs) are an important extension of CDMs. They model individuals’ status for each attribute to be continuous for measuring the partial mastery level, which relaxes the restrictive discrete-attribute assumption of classical CDMs. As a result, PM-CDMs often yield better fits for real-world data and refined measurement of the substantive attributes of interest. However, these models inherit some strong parametric assumptions from the traditional CDMs about the item response functions and, thus, still suffer from a significant risk of model misspecification. This paper proposes a generalized additive PM-CDM (GaPM-CDM) that substantially relaxes the parametric assumptions of PM-CDMs. This proposal leverages model parsimony and interpretability by modeling each item response function as a mixture of nonparametric monotone functions of attributes. A method for the estimation of GaPM-CDM is developed, which combines the marginal maximum likelihood estimator with a sieve approximation of the nonparametric functions. The new model is applicable under both confirmatory and exploratory settings, depending on whether prior knowledge is available about the relationship between observed variables and attributes. The proposed method is applied to two measurement problems from educational testing and healthcare research, respectively, and further evaluated and compared with PM-CDMs through extensive simulation studies.

A semi-parametric partial-mastery model that works in exploratory and confirmatory settings. Efficient MML estimation via stochastic approximation.

@article{ccardehu_arXiv2025, author = {Cárdenas-Hurtado, Camilo A. and Chen, Yunxiao and Moustaki, Irini}, doi = {https://doi.org/10.48550/arXiv.2511.20191}, month = nov, title = {A Generalized Additive Partial-Mastery Cognitive Diagnostic Model}, tldr = {A semi-parametric partial-mastery model that works in exploratory and confirmatory settings. Efficient MML estimation via stochastic approximation.}, year = {2025}, category = {pre-prints} }

Peer-Reviewed Publications

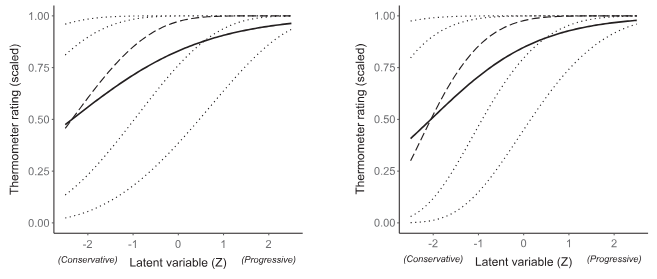

- Generalized Latent Variable Models for Location, Scale, and Shape parametersSep 2025

We introduce a general framework for latent variable modeling, named Generalized Latent Variable Models for Location, Scale, and Shape parameters (GLVM-LSS). This framework extends the generalized linear latent variable model beyond the exponential family distributional assumption and enables the modeling of distributional parameters other than the mean (location parameter), such as scale and shape parameters, as functions of latent variables. Model parameters are estimated via maximum likelihood. We present two real-world applications on public opinion research and educational testing, and evaluate the model’s performance in terms of parameter recovery through extensive simulation studies. Our results suggest that the GLVM-LSS is a valuable tool in applications where modeling higher-order moments of the observed variables through latent variables is of substantive interest. The proposed model is implemented in the R package glvmlss, available online.

A distributional latent variable model framework where the distributional parameters depend on the latent variables. We can model higher-order moments of observed items.

@article{ccardehu_Psychometrika2025, author = {Cárdenas-Hurtado, Camilo A. and Moustaki, Irini and Chen, Yunxiao and Marra, Giampiero}, doi = {https://doi.org/10.1017/psy.2025.7}, month = sep, number = {3}, pages = {932-956}, title = {Generalized Latent Variable Models for Location, Scale, and Shape parameters}, tldr = {A distributional latent variable model framework where the distributional parameters depend on the latent variables. We can model higher-order moments of observed items.}, volume = {90}, year = {2025}, category = {peer-reviewed} } - A Statistical Analysis of Heterogeneity on Labour Markets and Unemployment Rates in ColombiaCamilo A. Cárdenas-Hurtado, M. A. Hernández-Montes, and J. E. Torres-GorronJan 2015

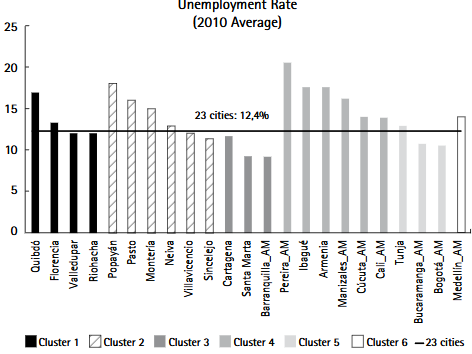

n this paper, we study the structural factors that determine the differences in unemployment rates and in labour market performance for Colombian cities. Using cross-sectional data for 23 metropolitan areas, we apply an extension of a principal axes method—Multiple Factor Analysis for Multiple Contingency Tables (MFACT)—in order to identify unobservable factors that are relevant when disentangling the heterogeneity observed among groups of variables considered explanatory of regional unemployment differentials. Our findings suggest that differences in qualified labour supply levels, participation incen-tives and age structure are important when it comes to understanding regional heterogeneity in terms of labour markets and unemployment rates in Colombia.

Multivariate analysis of unemployment rate heterogenity in Colombia. We use advanced PCA methods and hierarchical clustering.

@article{ccardehu_DyS2015, author = {Cárdenas-Hurtado, Camilo A. and Hernández-Montes, M. A. and Torres-Gorron, J. E.}, doi = {https://doi.org/10.13043/dys.75.4}, month = jan, number = {1}, pages = {153-196}, title = {A Statistical Analysis of Heterogeneity on Labour Markets and Unemployment Rates in Colombia}, tldr = {Multivariate analysis of unemployment rate heterogenity in Colombia. We use advanced PCA methods and hierarchical clustering.}, volume = {75}, year = {2015}, category = {peer-reviewed} }

Policy Papers

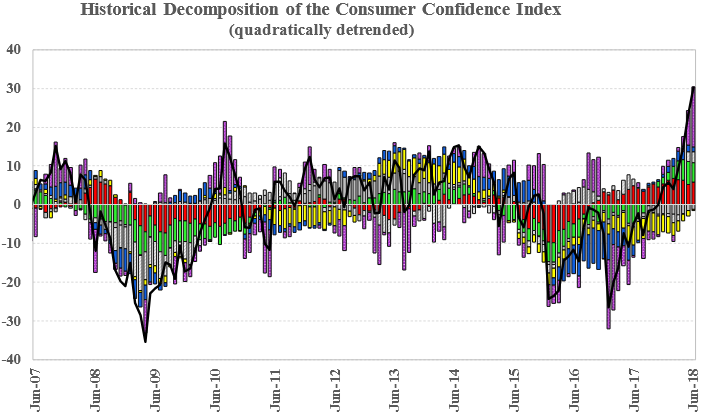

- Understanding the Consumer Confidence Index in Colombia: A structural FAVAR analysisCamilo A. Cárdenas-Hurtado, and M. A. Hernández-MontesFeb 2019

The consumer confidence index (CCI) is very relevant for economic analysis due to its timely publication and forecasting capacities. Although there is extensive literature on the link between CCI and macroeconomic aggregates, in particular with households’ consumption, few papers have studied the fundamental factors that explain the CCI behaviour. Actually, no attempt has been made for the Colombian case. In this paper we aim to fill this gap. We estimate a Structural Factor-Augmented VAR (SFAVAR) model and perform a historical decomposition (HD) on the CCI series to obtain the underlying structural innovations that drove the CCI dynamics over the past few years. Our findings suggest that the CCI responded to changes in the underlying determinants and to non-fundamental shocks possibly related to uncertainty periods and noneconomic, socio-political or electoral events. Moreover, a counterfactual analysis shows that households’ consumption forecasts improve when using the CCI series that are not affected by these non-fundamental shocks.

A structural factor-augmented VAR (SFAVAR) for the consumers’ confidence index in Colombia. We present a decomposition into structural determinants and political shocks.

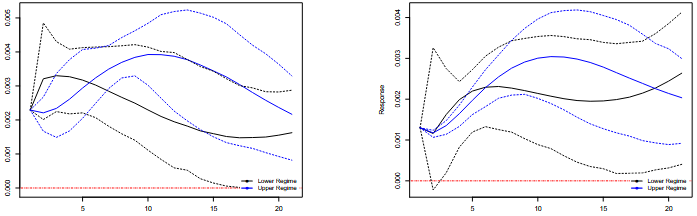

@article{ccardehu_BdE2019, author = {Cárdenas-Hurtado, Camilo A. and Hernández-Montes, M. A.}, doi = {https://doi.org/10.32468/be.1063}, month = feb, number = {1063}, title = {Understanding the Consumer Confidence Index in Colombia: A structural FAVAR analysis}, tldr = {A structural factor-augmented VAR (SFAVAR) for the consumers' confidence index in Colombia. We present a decomposition into structural determinants and political shocks.}, year = {2019}, category = {policy-papers} } - Asymmetric Effects of Terms of Trade Shocks on Tradable and Non-tradable Investment Rates: The Colombian CaseCamilo A. Cárdenas-Hurtado, A. L. Garavito-Acosta, and J. H. Toro-CórdobaJul 2018

Terms of trade (ToT) shocks drive business cycles and have direct impact on the macroeconomic equilibrium conditions in commodity-exporter countries. ToT shocks also affect the dynamics of other variables such as national income and relative prices, and consequently, cause agents and firms to adjust their saving, spending and investment decisions accordingly. The latter is of special interest because of its link with potential GDP and the capital stock of the economy, relevant concepts when assessing sustainable and long-run growth. In this document we explore how tradable and nontradable investment rates respond asymmetrically to ToT shocks. We estimate a Threshold VAR (TVAR) in which the ToT are the transition variable. The empirical results suggest the existence of two regimes (low and high ToT levels) and that ToT shocks have different effects on tradable and nontradable investment rates depending not only the direction of the shock, but also on the levels from which the shock departs.

A threshold VAR (TVAR) for tradable and non-tradable investment rates in Colombia. Generalized impulse response functions (GIRFs) to study dynamics.

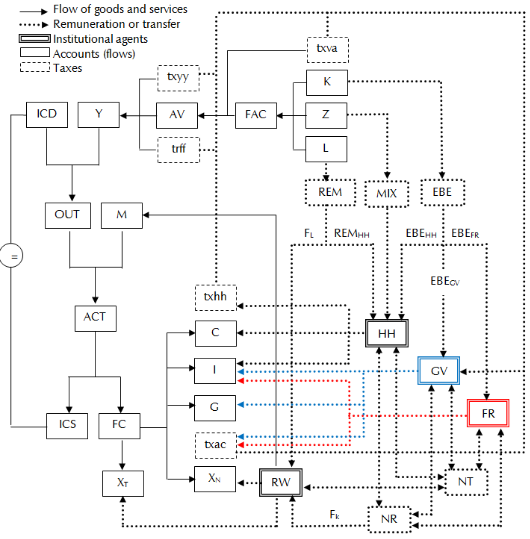

@article{ccardehu_BdE2018, author = {Cárdenas-Hurtado, Camilo A. and Garavito-Acosta, A. L. and Toro-Córdoba, J. H.}, doi = {https://doi.org/10.32468/be.1043}, month = jul, number = {1043}, title = {Asymmetric Effects of Terms of Trade Shocks on Tradable and Non-tradable Investment Rates: The Colombian Case}, tldr = {A threshold VAR (TVAR) for tradable and non-tradable investment rates in Colombia. Generalized impulse response functions (GIRFs) to study dynamics.}, year = {2018}, category = {policy-papers} } - A Macro CGE Model for the Colombian EconomyA. M. Velasco, and Camilo A. Cárdenas-HurtadoJun 2015

This paper presents the construction of a tailor-made Macro Computable General Equilibrium Model for the Colombian economy that satisfies Banco de la República’s macroeconomic programming and forecasting interests. Using information on the national accounts divulged by the National Statistics Department (DANE), we set an easily updatable Macro Social Accounting Matrix that serves as a starting point for the model parameters calibration and estimation.

A Macro CGE Model for the Colombian Economy calibrated using national accounts. It allows for structural forecasting of macro-trends for a small open economy.

@article{ccardehu_BdE2015, author = {Velasco, A. M. and Cárdenas-Hurtado, Camilo A.}, doi = {https://doi.org/10.32468/be.863}, month = jun, number = {863}, title = {A Macro CGE Model for the Colombian Economy}, tldr = {A Macro CGE Model for the Colombian Economy calibrated using national accounts. It allows for structural forecasting of macro-trends for a small open economy.}, year = {2015}, category = {policy-papers} }